The Age of Compute: How AI and Data Centers Rewired Global Energy Investment

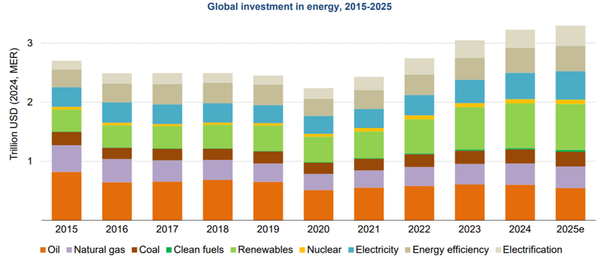

Global energy investment hits $3.3 trillion in 2025, with two-thirds ($2.2 trillion) now flowing to clean energy. The IEA warns that AI and data centers are reshaping demand, potentially consuming 1,000 TWh by 2030 and driving a new “Age of Electricity and Intelligence.”

The Age of Electricity Meets the Age of Constraint: IEA’s Energy Technology Perspectives 2026 Describes a System in Transition

Energy is shifting from a single constraint (cost) to a multi-constrained system—power, materials, supply chains, and policy. Clean tech is scaling on economics, but fragility is rising. The transition now hinges not just on deployment, but on aligning constraints across the system.

Brandon Owens

The Shadow Grid Doctrine: The United States Is Building a Second Energy System for Artificial Intelligence

The White House AI framework accelerates infrastructure at unprecedented speed—but exposes 10 systemic risks, from rising grid fragmentation and cost shifting to reliability, market and governance gaps, as a “Shadow Grid” emerges outside traditional oversight.

Brandon Owens

Shadow Grid: The Grid Is Splitting in Two

Data center developers are building a parallel “shadow grid” to bypass delays and costs. With 47 GW emerging—rivaling grid builds—this system is largely invisible to planners. FERC’s response may unintentionally push more operators fully off-grid, deepening coordination and reliability risks.

Michael Leifman

From Automation to Control: Architecting the Software-Defined Grid

The grid is shifting from hardware-based control to software-defined systems. AI, electrification, and distributed energy are driving this change, introducing new risks and requiring integrated, adaptive control across sensing, communication, and computation layers.

Brandon Owens

The Shadow Grid: AI’s Hidden Energy Network and the Crisis of Infrastructure Visibility

AI data centers are driving a surge in electricity demand and spawning a “shadow grid” of private power plants. Built outside traditional planning, this hidden infrastructure erodes visibility over the energy system and creates new challenges for governance and reliability.

Brandon Owens