The shadow grid is not emerging from legislation or long-range planning. It is being built, contract by contract, by data center developers solving a simpler problem: how to secure power on their own terms. Faced with interconnection delays, uncertain timelines, and rising costs, they are assembling a parallel system of generation, storage, and control directly on or adjacent to their campuses. It runs alongside the traditional grid but is not governed by it in the same way. It is built for certainty, speed, and autonomy—not participation.

On the ground, this shift is already visible. In Ohio and New Mexico, in Tennessee and Utah, natural gas turbines, solar arrays, and battery systems are being designed into data center campuses from the outset. These are not backup resources waiting for an outage. They are primary infrastructure, sized and configured for continuous operation. Some sites maintain selective ties to the grid, drawing power when it is advantageous. Others are engineered to operate largely on their own. What is taking shape is a distributed, privately controlled layer of energy infrastructure that mirrors the grid in function but not in form.

To understand the magnitude of this buildout, AIxEnergy assembled a national dataset from state air permits, siting dockets, county filings, corporate disclosures, earnings calls, and equipment procurement signals, combined with probability-weighted commercial operation timelines. The numbers tell a precise story. Between 2026 and 2028, expected shadow gas additions—47 gigawatts—closely track the 46 gigawatts of gas planned for grid connection. But the symmetry does not hold. In 2027, probability-weighted shadow capacity reaches 21.7 gigawatts, exceeding the 12.3 gigawatts slated for the grid. Across three years, these projects represent 186 gigawatts of privately developed capacity exposure—generation that exists, but does not fully register in the models planners rely on.

Most of this system remains difficult to see. It does not pass cleanly through interconnection queues. It does not fully appear in resource adequacy plans. And it sits only partially inside the datasets used to forecast how the grid will evolve.

In a previous AIxEnergy article, The Shadow Grid: How Regulatory Seams Are Reshaping American Power, Brandon Owens grounds the governance problem in a simple observation: grid regulators and operators depend on interconnection queues, resource adequacy plans, and capacity forecasts to understand the system they are responsible for managing. The shadow grid introduces blind spots in all three. The Federal Energy Regulatory Commission’s December 2025 order is a direct response to that problem. In important respects, it is the right response. But it carries an unintended consequence that has not been fully examined. By raising the cost and complexity of grid participation for large operators, it creates a financial incentive to bypass the system altogether.

The risk is not simply more private generation. It is a version of the shadow grid that becomes structurally invisible—outside planning processes, outside reliability frameworks, and increasingly outside coordination. To make that risk clear, it is necessary to be precise about what the shadow grid actually is. Not all behind-the-meter configurations are the same. And the policy consequences depend on which version of the system is actually emerging.

The shadow grid is not one thing

When people talk about the shadow grid, they typically mean data centers that generate their own power behind the meter rather than drawing it from the grid. But the FERC order and PJM’s compliance filings reveal at least four distinct configurations, each with a different regulatory treatment, a different resource adequacy impact, and a different risk profile for investors.

Truly islanded generation

The first and most extreme configuration is zero grid connection: no transmission service taken, no Network Load designation, no PJM obligation to serve the load. PJM has no visibility into this load at all. It does not exist in the planning framework, and because PJM cannot see it, there is no PJM-imposed cap on it.

“Option 5”: grid-connected with protections

The second configuration is what PJM calls “Option 5” in its co-location filings: a grid-connected arrangement where physical protections prevent grid energy from flowing to the load under normal conditions, but where PJM backup service remains available and the load retains its Network Load designation. PJM does plan for this load, and the operator carries obligations. Because this configuration does not carry reserves equal to the installed reserve margin, allowing it to grow unchecked degrades PJM’s loss of load expectation (LOLE), the standard measure of the probability the grid will be unable to serve demand. PJM accommodates “Option 5” through a 2006 settlement agreement that relaxed the LOLE standard from 1-in-10 to 1-in-9.5 years, and caps this configuration at approximately 2,000 MW system-wide, of which roughly 1,300 MW are already in use. This cap is relevant to the perverse incentive argument below.

Large BTM with grid connection

The third configuration is the primary target of FERC’s December 2025 order: large behind-the-meter generation with a full grid connection. Here, a data center generates some of its own power but takes Network Integration Transmission Service (NITS) from the grid and carries a full Network Load designation, meaning PJM has a legal obligation to serve it. Under existing rules, PJM plans for the net load. If a 500 MW data center has a 500 MW behind-the-meter generator, it appears in PJM’s planning as zero net load. PJM must serve it but cannot plan the resources to do so. FERC found that “loads with BTMG are not fully accounted for in resource adequacy planning,” and the behind-the-meter generator that offsets the capacity obligation cannot participate in PJM’s capacity market to fill that planning gap. Manual 14G states this explicitly.

FERC’s proposed remedy is a materiality threshold: facilities above a certain size lose the ability to net their behind-the-meter generation against their load obligation. The full load reappears in PJM’s resource adequacy planning, and PJM can plan for what it must serve. That is the right outcome, if the threshold holds.

Full co-location: the reference point

Before introducing the fourth configuration, it is worth establishing what full grid participation looks like. In a true co-location arrangement, the generator interconnects directly to the grid as a capacity resource, the load takes full NITS service, and both sides are fully visible to PJM’s planning and capacity market. The load-serving entity procures capacity for the full gross load. There is no governance gap. This is the reference point against which the intermediate configurations should be evaluated.

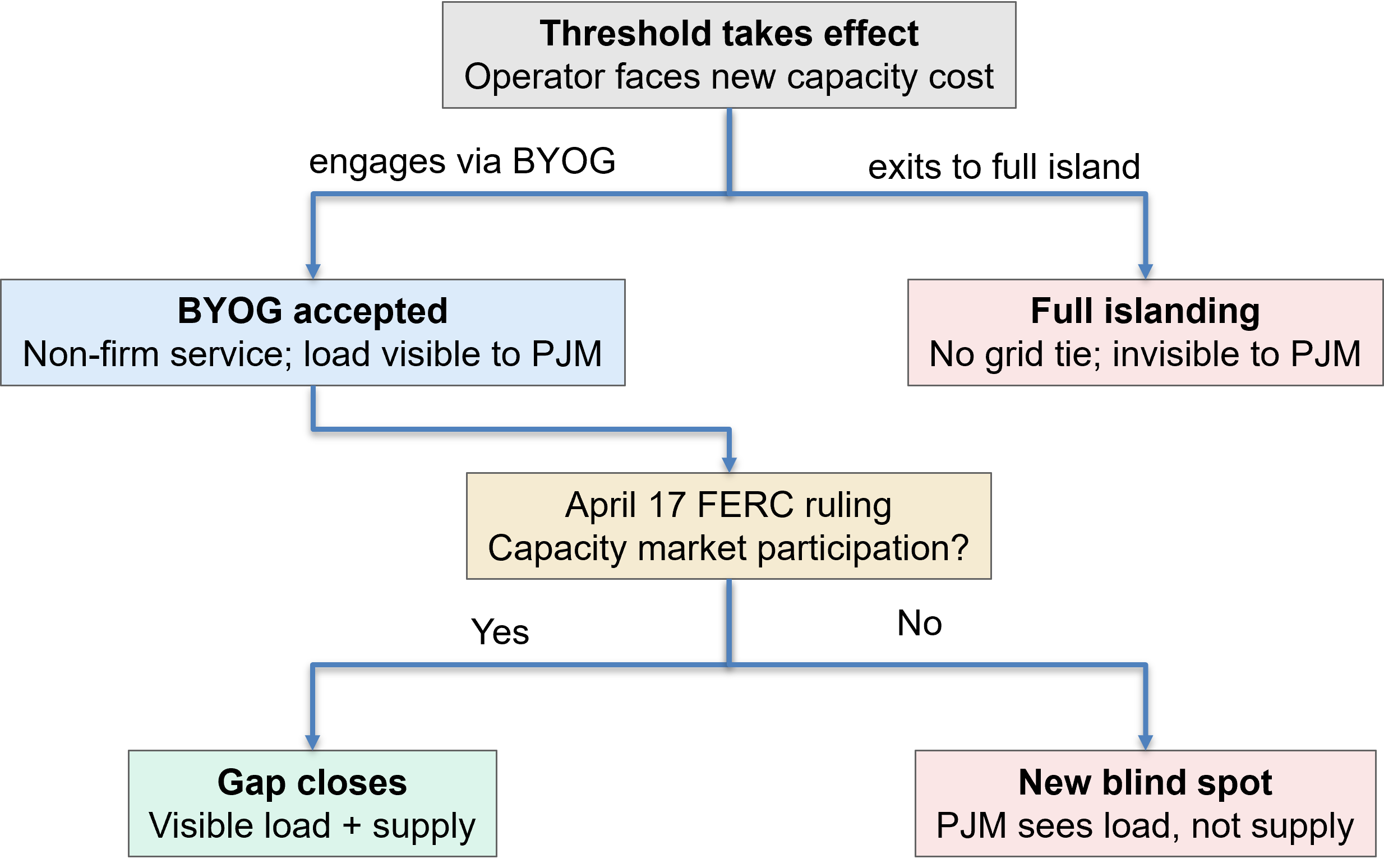

BYOG: the proposed bridge

The fourth configuration sits between large BTM and full co-location. Bring Your Own Generation, or BYOG, was introduced in PJM’s January 2026 Board Decisional Letter as an expedited interconnection path. Under BYOG, a data center commits to bring new generation capacity to the system (through new-build facilities, uprates to existing generators, or PPAs) in exchange for faster interconnection and acceptance of curtailment risk rather than full firm service. The generation does not have to be physically behind the meter or on-site; the defining trade is speed in exchange for interruptibility.

(The formula of speed in exchange for a commitment is not new. The 2025 uncertainty framework published on this platform proposed using expedited interconnection as an incentive for tangible carbon reduction commitments. BYOG uses the same mechanism but substitutes curtailment acceptance for environmental performance.)

BYOG differs from full co-location in an important respect. In a true co-location arrangement, the generator interconnects directly to the grid as a capacity resource and the load takes full NITS service, with both sides visible to PJM’s planning. BYOG accepts interruptibility in place of firm service and does not require the generator to offer into PJM’s capacity market, at least not yet. The governance question BYOG raises is this: without a requirement to offer into PJM’s capacity market, the generation a data center “brings” may never become visible to PJM’s supply-side planning. The facility remains Network Load, PJM retains its service obligation, and the threshold change makes the load visible on the demand side. But if the BYOG generation stays off PJM’s books, the supply side remains in the shadows. BYOG could, without the right design, replicate the very governance problem it was meant to solve.

The table below summarizes the configurations from least to most grid engagement.

| Configuration | PJM Obligation | What It Means |

|---|---|---|

| Truly islanded | None | No grid connection. Invisible to PJM. No planning visibility and no system cap applies. |

| “Option 5” | Limited (backup only) | Grid-connected with protections. PJM sees the load but only as backup. Capped at roughly 2,000 MW system-wide. |

| Large BTM (above threshold) | Full | Netting eliminated. PJM must plan for the full gross load. Primary target of the FERC remedy. |

| BYOG | Full | Faster interconnection in exchange for interruptibility. Load is visible, but supply-side visibility may remain unresolved. |

| Full NITS / co-location | Full | Both load and supply are fully visible to PJM. Fully integrated into planning and capacity markets. |

A threshold that may not hold

FERC’s December 2025 order directed PJM to propose a materiality threshold above which BTM netting no longer applies. PJM’s February 23, 2026 compliance filing proposed 50 MW. FERC has not yet accepted or rejected that level, and the outcome is far from certain.

If FERC sets the threshold significantly higher than 50 MW, or rejects PJM’s proposal, a large portion of the hyperscale buildout remains in the netting-makes-both-invisible situation indefinitely. The resource adequacy gap Owens documented and FERC correctly diagnosed does not get fixed. Most coverage of this rulemaking treats the threshold as settled. It is not, and investors underwriting BTM projects on the assumption that the regulatory framework will stabilize around 50 MW should treat that assumption with care.

FERC is right, but creates a new risk

Assuming the threshold takes effect near 50 MW, the order correctly addresses the resource adequacy and cost-causation problems created by large BTM loads operating outside the planning framework. The risk is not that FERC got the diagnosis wrong. It is that the remedy creates a financial incentive to exit the grid entirely.

When netting is eliminated for a large BTM facility, the load-serving entity (LSE) responsible for that customer must now procure capacity for the full gross load rather than the net. The cost of that additional procurement is allocated across LSEs through the Locational Reliability Charge, PJM’s mechanism for recovering capacity commitments from load-serving entities based on their load obligations. Whether and how that cost ultimately reaches the specific data center customer depends on the retail tariff structure and the contract between the LSE and its customer. In competitive retail markets, LSEs typically pass incremental costs through. At PJM’s current capacity price of $329/MW-day, the order of magnitude of that additional cost for a 500 MW facility is approximately $60 million annually. For investors who underwrote the BTM structure specifically to avoid capacity costs, this is not a routine regulatory adjustment. It is a fundamental repricing of the investment thesis.

For an operator who can make the physics work (who can genuinely island the facility with zero grid connection and no Network Load designation), exiting the framework entirely may be the rational response. The result would be no capacity charges, no NITS fees, no ancillary service obligations. The FERC order, by raising the cost of remaining in the framework, inadvertently creates a financial incentive to become exactly what Owens’ series identifies as the core governance problem: a facility genuinely invisible to the institutions designed to plan around it.

This is where the 2,000 MW cap under PJM’s 2006 settlement becomes relevant. That cap applies to “Option 5,” the grid-connected-with-protections configuration where PJM retains a backup service obligation and can still see the load. If the financial pressure of the FERC order pushes operators toward genuine islanding with zero grid connection (outside even “Option 5”), that cap provides no constraint whatsoever. The reliability framework it represents would face pressure it was never designed to absorb.

Two consequences of scaled full islanding

The first is carbon accountability. Truly islanded gas generation is structurally exempt from every decarbonization mechanism: utility RPS compliance, state clean energy accounting, carbon inventories. It is not interconnected, not metered by utilities, and not visible to any regulatory framework designed to track and reduce emissions. Owens’ bifurcated carbon ledger does not just persist under this scenario. It expands.

The second is gas-electric coordination failure, the piece of the shadow grid story that has not been told. Today, gas and electric market coordination happens through the dispatch stack and firm transportation contracts. PJM knows which gas-fired generators need fuel and can dispatch alternatives when they lose it. The central lesson of Winter Storm Uri was that this coordination can fail catastrophically, but at least the failure was visible and could be diagnosed.

Truly islanded data center power plants break this coordination in a way that is fundamentally harder to diagnose. They are invisible to PJM, so it cannot dispatch alternatives when an islanded generator loses fuel. They may not hold firm gas transportation contracts, since there is no regulatory pressure requiring them to do so. Unlike grid-connected generators, they have no place in the coordination framework that allocates fuel supply during stress events. The coordination failure is acute precisely when coordination matters most.

The April 17 fork

BYOG is designed as the alternative to full islanding: commit to bring generation, accept interruptibility, and receive faster interconnection. Whether it actually closes the resource adequacy gap depends on the FERC paper hearing reply brief deadline of April 17, 2026 (docket EL25-49-000), which will determine whether large BYOG generators must offer into PJM’s capacity market.

If FERC requires capacity market participation, the generation committed through BYOG becomes visible to PJM’s supply-side planning alongside the load it already sees. The resource adequacy gap closes. This moves BYOG meaningfully toward the full co-location model: visible load, visible supply.

If FERC does not require it, the threshold change creates a problem that is in one respect worse than today. Currently, PJM is blind to both the load and the supply for large BTM configurations. Under the threshold change without capacity market participation requirements, PJM sees the full load obligation but the supply covering it remains invisible. Planning is blind on only one side, and it is the wrong side. Most investors are treating the April 17 outcome as settled. It is not.

The standby charge gap

The actual ratepayer protection mechanism, where it exists, is state utility commission standby charge tariffs. When a large customer self-supplies but remains connected to the grid for backup or supplemental power, a properly designed standby charge requires payment toward grid infrastructure costs even when the customer is not actively drawing power. The charge has two components. The first is availability: the grid must be built and maintained to serve that customer at full load whenever its private generation fails. The second is system stability: large BTM generators affect grid frequency, voltage support, and reactive power balance continuously, whether or not they are drawing power. These are real costs that neighboring customers currently bear without recovery.

Virginia is the most consequential near-term jurisdiction. In November 2025, the State Corporation Commission approved Dominion Energy’s new GS-5 rate class for customers consuming over 25 MW and required minimum demand charges to protect ratepayers from infrastructure costs. But the SCC explicitly deferred the harder question of how to assign generation system costs to data centers, asking Dominion to return with a proposal in its 2027 rate case. That deferral is where the standby charge gap lives. For investors evaluating BTM projects in Virginia and similar jurisdictions, how the 2027 case resolves is a material open question, and the direction of resolution is not favorable to the current cost structure.

The answer that isn’t winning yet

The debate over the shadow grid has been conducted almost entirely in terms of what is wrong with BTM gas. Less attention has gone to a constructive model that already exists and resolves the carbon, reliability, ratepayer, and coordination problems simultaneously while meeting the speed requirements of the AI buildout.

The Power Couples framework, developed by Uday Varadarajan and colleagues at RMI and now being commercialized through Colectric, pairs a large electricity consumer with new-build solar, wind, and storage resources sized to meet the on-site load, sited near an existing generator with approved grid interconnection. The existing plant’s surplus interconnection capacity provides grid access in months rather than years. Physical safeguards ensure no net grid power withdrawal, eliminating the resource adequacy concern entirely. The arrangement stays inside the institutional framework, visible to planners, countable in resource adequacy studies, and subject to the regulatory processes that BTM gas is bypassing.

RMI’s analysis finds that over 50 GW of data center load could be served this way at 88% carbon-free energy on average, with over 30 GW available below $100/MWh. Colectric lists Apple, Meta, and Akamai among its incubation partners. The hyperscalers driving the BTM gas buildout are, in some cases, the same companies that are supporting the alternative. One honest constraint: the Power Couples model depends on the geographic distribution of existing generators with surplus interconnection, and the AI buildout’s concentration in climate-stressed Southern geographies creates real siting limits that any co-location model must navigate.

Power Couples is not currently winning primarily because the regulatory framework has not yet made the full costs of BTM generation visible to the operators who choose it. When the materiality threshold takes effect, when standby charges reflect grid stability costs, and when gas price assumptions embedded in long-lived BTM capital assets are stress-tested against a globalizing gas market, the Power Couples economics improve materially relative to every segment of the shadow grid. The FERC order is a step in that direction. Its blind spot is the fully islanded model it may inadvertently accelerate.

Three near-term levers

April 17, 2026 is the most time-sensitive decision point. The FERC paper hearing (docket EL25-49-000) will determine whether BYOG generators must participate in PJM’s capacity market. A ruling requiring participation would close the visible-load-invisible-supply problem the threshold change otherwise creates, and would signal that grid engagement is the viable path rather than a cost to be avoided.

Virginia’s 2027 SCC rate case is the second lever. The SCC’s November 2025 order deferred the question of how to assign generation system costs to data centers. When Dominion returns with a proposal, the outcome will determine whether standby charge-equivalent obligations are imposed on large BTM customers in the most important data center market in the country, and will set a template other states follow.

Disclosure is the third lever. The data center uncertainty framework published on this platform in November 2025 proposed granular behind-the-meter generation and storage plans filed with utilities and ISOs. That requirement would make the shadow grid visible to the institutions currently blind to it, and give gas pipeline operators the information they need to coordinate fuel supply for loads they cannot currently see.

Owens’ series calls for enhanced reporting requirements, expanded regional planning roles, and AI transparency mandates for grid management algorithms, the right long-run responses. The three levers above are more immediately tractable and are where the most consequential decisions are being made right now.

The shadow grid is not an accident of technology. It is the outcome of rules that stopped at the edge of the grid while the system itself kept expanding. Those edges are now visible. Some are being closed. Others remain open in ways that matter more with each new facility that steps outside the frame. The risk is not that power moves off the grid. It is that governance does not follow it.

If the incentives continue to favor full islanding, if fuel coordination remains fragmented, if cost recovery lags behind physical reality, then the system will evolve into something planners can no longer fully see—much less manage.

The next failure will not begin as a shortage of energy. It will begin as a gap between what the system is responsible for and what it can observe. And by the time that gap is visible, it will already be structural.

Michael Leifman is the founder of Tenley Energy Innovation LLC and writes about energy markets and AI infrastructure at MichaelLeifman.Substack.com.