Semiconductor manufacturing depends on some of the world’s most sophisticated equipment, but very dependent on a material most investors and policymakers have never heard of. This summer, that material is tungsten hexafluoride, or WF6: a toxic, corrosive, odorless specialty gas used to deposit tungsten in semiconductor manufacturing. 3

By June, a stark story had spread through the semiconductor trade coverage. Kanto Denka Kogyo and Central Glass, two major Japanese specialty-chemical producers, were said to be running out of tungsten feedstock and preparing to stop WF6 production around July 1. Later reports hardened the warning into a declaration that both companies had permanently exited production, removing roughly a quarter of global capacity. 7,8

However, on June 25, Central Glass said it had secured the raw materials needed to meet customer orders and was continuing to supply its semiconductor specialty gases. Kanto Denka’s May 25 financial briefing reported that WF6 sales had increased on higher volumes and price adjustments, forecast substantially higher specialty-gas sales in the fiscal year ending March 2027, and showed continuing WF6 activity at its Chinese affiliate. 1,2

That correction does not make the supply problem disappear. As it turns out, materials can remain legal to export, and a gas producer can remain in operation, while feedstock restrictions, price spikes, inventory risk, and long qualification cycles still create a serious bottleneck.

Why WF6 Matters

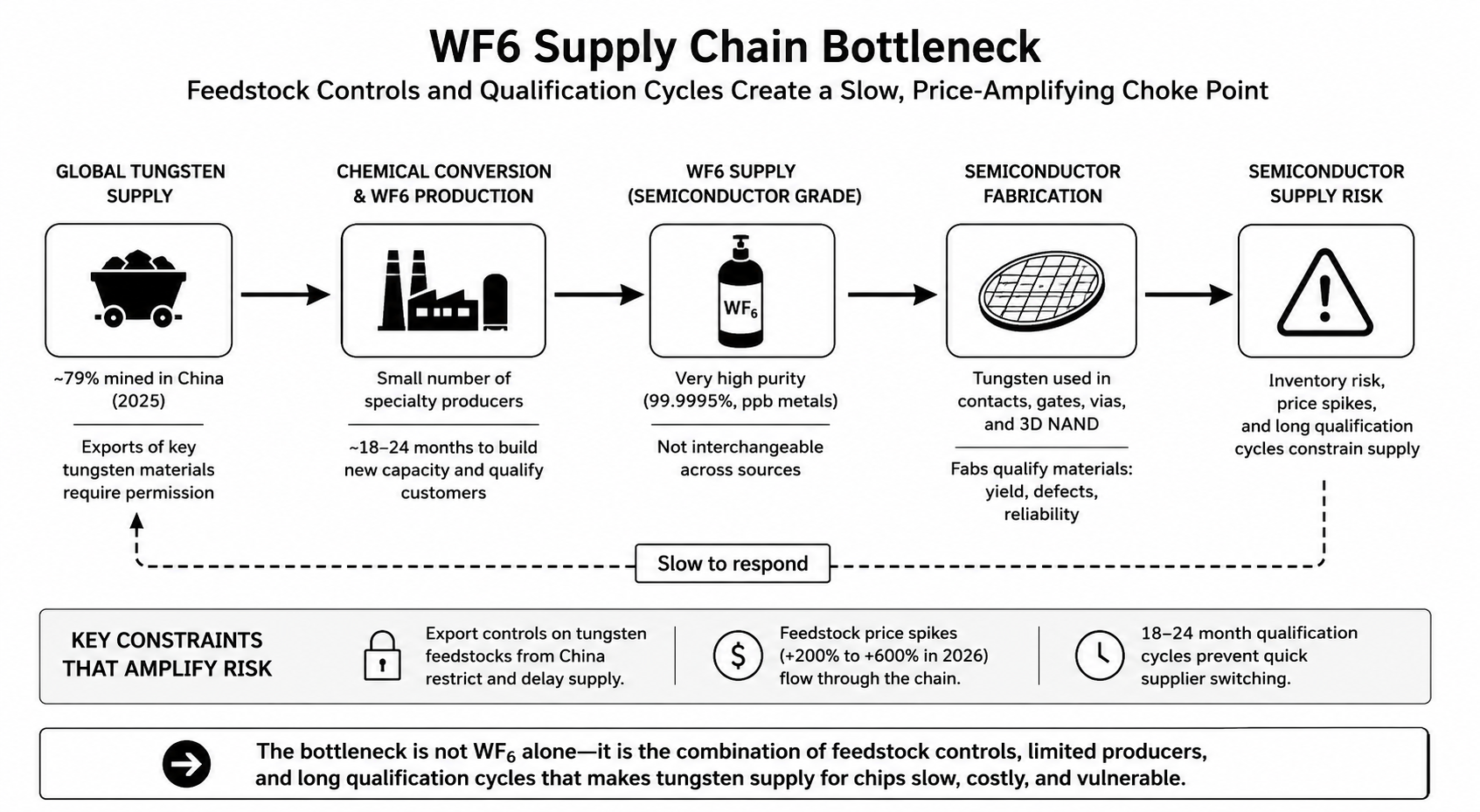

WF6 is used in deposition processes that form tungsten films and features inside logic and memory devices. Tungsten has long been used where copper is unsuitable, including contacts, gates, vias, and 3D NAND word lines. Semiconductor-grade material is extraordinarily pure: commercial products are offered at 99.9995 percent purity, with individual metallic contaminants specified at parts-per-billion-by-weight levels. 3,4,10

Semiconductor fabs qualify materials against process recipes, tool conditions, defect levels, electrical performance, yield, and long-term reliability. A new source of WF6 is therefore not interchangeable with an existing source in the way one barrel of a commodity grade might substitute for another. Trade reports put new-capacity buildout and customer qualification cycles at roughly 18 to 24 months. The response time of a qualified supply chain is much slower than the response time of a spot market. 8

While tungsten remains deeply embedded in qualified manufacturing flows, and replacing it quickly is difficult, molybdenum is already moving into specific metallization applications. Lam Research said in February 2025 that its molybdenum atomic-layer-deposition platform was in volume production, including early adoption in 3D NAND and advanced logic. Kioxia has demonstrated a fluorine-free molybdenum word-line process for 3D flash memory, and Applied Materials said in June 2026 that a molybdenum etch system had been validated in high-volume manufacturing. Substitution is real, but cannot be treated as an emergency drop-in replacement. 10,11,12

Supply

On February 4, 2025, China’s Ministry of Commerce and General Administration of Customs imposed export controls on selected tungsten-related items under Decision No. 10 of 2025. The covered list included ammonium paratungstate, tungsten oxide, certain tungsten carbide products, specified solid tungsten products and alloys, and related production technologies. The regime requires exporters to obtain permission. 5

China then tightened controls on dual-use trade involving Japan in early 2026. Chinese customs data cited by Fastmarkets show that exports of high-purity tungsten powder to Japan fell to zero for three consecutive months from February through April 2026. Yet WF6 itself was not included on the cited dual-use control list. China exported 210.9 metric tons of WF6 from January through May 2026, including 28.02 metric tons to Japan. 7

The US Geological Survey estimates that China mined 67,000 metric tons of tungsten in 2025 out of a world total of 85,000 metric tons, or about 79 percent. In 2024, China produced 67,000 metric tons out of 82,000, or about 82 percent. 6

The United States has had no commercial tungsten mine production since 2015, although USGS reports that seven US companies can convert concentrates, ammonium paratungstate, tungsten oxide, or scrap into tungsten powders, carbide powders, metal, or chemicals. Outside China, mining is beginning to diversify. Almonty Industries began mining at the Sangdong project in South Korea in March 2026, with a second-phase expansion expected in 2027. But new mine output and qualified electronic-grade specialty gas are separated by conversion, purification, gas production, logistics, and fab qualification.6,9

Prices

Reuters reported in late April that ammonium paratungstate prices in Rotterdam had moved above $3,000 per metric ton unit, more than 200 percent higher than at the start of 2026. Fastmarkets assessed Chinese export APT at $2,600 to $3,200 per metric ton unit on July 1, roughly 600 percent above its level a year earlier. 7,9

WF6 pricing is less transparent. There is no widely used public global benchmark for semiconductor-grade material, and reported prices can mix grades, contract terms, and shipment composition. Chinese customs data cited by TrendForce put the average April 2026 WF6 export unit value at $149.79 per kilogram, 28.33 percent higher than a year earlier and 203.83 percent higher than in March. That month-to-month jump should not be read as a clean spot-price index, but it illustrates the volatility entering the chain. Separately, The Elec reported in October 2025 that several suppliers had notified South Korean chipmakers of WF6 price increases of 70 to 90 percent for 2026. 8,13

Semiconductor buyers can absorb higher material costs for a time because specialty gases represent a small share of the value of a finished advanced chip. But once inventory buffers shrink, the relevant question is whether alternate gas supply has already been qualified.

AI Demand

WF6 is used across logic, DRAM, NAND, and 3D NAND manufacturing. AI infrastructure increases demand for advanced logic and high-bandwidth memory and contributes to strong capital spending across semiconductor manufacturing. But the tungsten squeeze reflects the collision of broad semiconductor demand, more demanding device structures, constrained upstream tungsten flows, and a specialty-gas market with limited transparency and slow qualification cycles. 3,4,7

Higher layer counts in 3D NAND make word-line metallization more demanding, but a 200-layer device does not imply a simple one-for-one count of 200 separate WF6 deposition cycles. Kioxia’s work on molybdenum substitution focuses on the electrical resistance, embeddability, fluorine residue, and leakage challenges that intensify as 3D flash structures scale. 11

This matters because if the problem is described as a single gas suddenly disappearing, the answer appears to be emergency procurement. If the problem is understood as a layered dependency, the response has to include feedstock mapping, conversion capacity, supplier qualification, inventory policy, recycling, and alternative process technologies.

The WF6 episode exposes four linked weaknesses in the semiconductor supply chain:

· First, geographic diversification can be superficial. A fab may buy from suppliers headquartered in Japan, South Korea, Europe, or the United States and still be exposed to the same upstream Chinese feedstock. Resilience analysis has to trace across supply chains.

· Second, an alternate supplier that exists on paper but has not been qualified on the relevant process is not usable capacity during a crisis. The semiconductor industry treats tool capacity as strategic.

· Third, the United States and allied countries can add tungsten production and still remain vulnerable if conversion, high-purity chemical production, packaging, analytical capability, and semiconductor qualification remain concentrated elsewhere.

· Fourth, substitution needs careful attention to detail. Molybdenum is already displacing tungsten in selected applications because device scaling itself is creating technical reasons to change metals.

Conclusion

Central Glass says it is continuing supply. Kanto Denka has reported higher WF6 sales and is forecasting growth in specialty gases. Chinese WF6 exports have continued. The question is how long an opaque, concentrated supply chain can absorb feedstock restrictions, extraordinary price movements, and slow qualification cycles, while semiconductor investment remains strong. 1,2,7

AI buildout depends on industrial chains several tiers upstream: specialty gases, photoresists, precursor chemicals, high-purity metals, substrates, packaging materials, and the equipment needed to make all of them. Their markets are small relative to the systems they enable.

The semiconductor industry has spent decades reducing defect rates and increasing efficiency by narrowing materials specifications and qualifying tightly controlled process flows. Those practices are essential to yield. They also make rapid supplier substitution difficult. Resilience, what we have previously termed “pre-logistics” in the military realm, has to be built before the shortages arise.

Notes and Sources

1. Central Glass Co., Ltd., “Regarding the Supply Status of Specialty Gases for Semiconductors,” June 25, 2026. https://www.cgc-jp.com/news/20260625180000.html

2. Kanto Denka Kogyo Co., Ltd., “Financial Results Briefing for the Fiscal Year Ended March 31, 2026,” May 25, 2026, esp. pp. 6, 13, 18, and 20. https://finance-frontend-pc-dist.west.edge.storage-yahoo.jp/disclosure/20260525/20260525546165.pdf

3. EMD Electronics, “Tungsten Hexafluoride Megaclass”; SK ecoplant materials, WF6 product specifications. https://www.emdgroup.com/en/expertise/semiconductors/offering/tungsten-hexafluoride-megaclass.html ; https://www.sk-materials.com/new/kor/html/products/wf6.asp

4. SK ecoplant materials, WF6 product information and impurity specifications. https://www.sk-materials.com/new/kor/html/products/wf6.asp

5. International Energy Agency, “Decision to Implement Export Controls on Tungsten, Tellurium, Bismuth, Molybdenum and Indium Related Items,” last updated May 5, 2025. https://www.iea.org/policies/26795-decision-to-implement-export-controls-on-tungsten-tellurium-bismuth-molybdenum-and-indium-related-items

6. US Geological Survey, Mineral Commodity Summaries 2026: Tungsten, February 2026. https://pubs.usgs.gov/periodicals/mcs2026/mcs2026-tungsten.pdf

7. Fastmarkets, “AI Specialty Gas Tightness Drives China’s Best-Performing A-Share in H1,” July 7, 2026. https://www.fastmarkets.com/insights/ai-specialty-gas-tightness-drives-chinas-best-performing-a-share-in-h1/

8. TrendForce, “Key Semiconductor Gas WF6 Prices Reportedly Surge Over 200% as Supply Tightens Ahead of Japan Output Cuts,” June 12, 2026. https://www.trendforce.com/news/2026/06/12/news-key-semiconductor-gas-wf%E2%82%86-prices-reportedly-surge-over-200-in-china-as-supply-tightens-ahead-of-japan-output-cuts/

9. Reuters, “Tungsten Breaks Records as China Export Curbs, Military Demand Boost Investment,” April 29, 2026; Reuters, “Tungsten Rises to Record Highs as Export Curbs Turn Up Supply Heat,” January 29, 2026. https://www.reuters.com/world/asia-pacific/tungsten-breaks-records-china-export-curbs-military-demand-boost-investment-2026-04-29/ ; https://www.reuters.com/world/americas/tungsten-rises-record-highs-export-curbs-turn-up-supply-heat-2026-01-29/

10. Lam Research, “Lam Research Ushers in New Era of Semiconductor Metallization with ALTUS Halo for Molybdenum Atomic Layer Deposition,” February 19, 2025. https://investor.lamresearch.com/2025-02-19-Lam-Research-Ushers-in-New-Era-of-Semiconductor-Metallization-with-ALTUS-R-Halo-for-Molybdenum-Atomic-Layer-Deposition

11. Kioxia, “Fluorine-Free Word Line Molybdenum Process for Enhancing Scalability and Reliability in 3D Flash Memory,” September 24, 2024. https://www.kioxia.com/en-jp/rd/technology/topics/topics-71.html

12. Applied Materials, “Applied Materials Unveils Deposition and Selective Etch Systems to Advance 3D Chip Scaling,” June 15, 2026. https://ir.appliedmaterials.com/news-releases/news-release-details/applied-materials-unveils-deposition-and-selective-etch-systems/

13. The Elec, “Chipmakers Samsung and SK Hynix Face WF6 Gas Price Hike,” October 28, 2025. https://www.thelec.net/news/articleView.html?idxno=5468