The map of American data center development is being redrawn in public hearings, zoning rooms, utility dockets, and state legislatures. As of June 2026, fourteen states had considered or were considering moratoria on data centers. In the first quarter of the year, Data Center Watch counted at least 75 U.S. projects, representing roughly $130 billion in proposed investment, that were blocked or delayed amid local opposition. Its count of active opposition groups had spread to 49 states.1, 2

Reducing that backlash to NIMBYism misses the harder infrastructure problem underneath. Communities are being asked to absorb facilities whose scale, power requirements, water demands, backup systems, tax arrangements, and land-use footprint can alter the trajectory of a place. A town that hesitates before accepting a 500 MW or 1 GW campus is not necessarily rejecting digital infrastructure. It may be rejecting the terms on which that infrastructure has arrived.

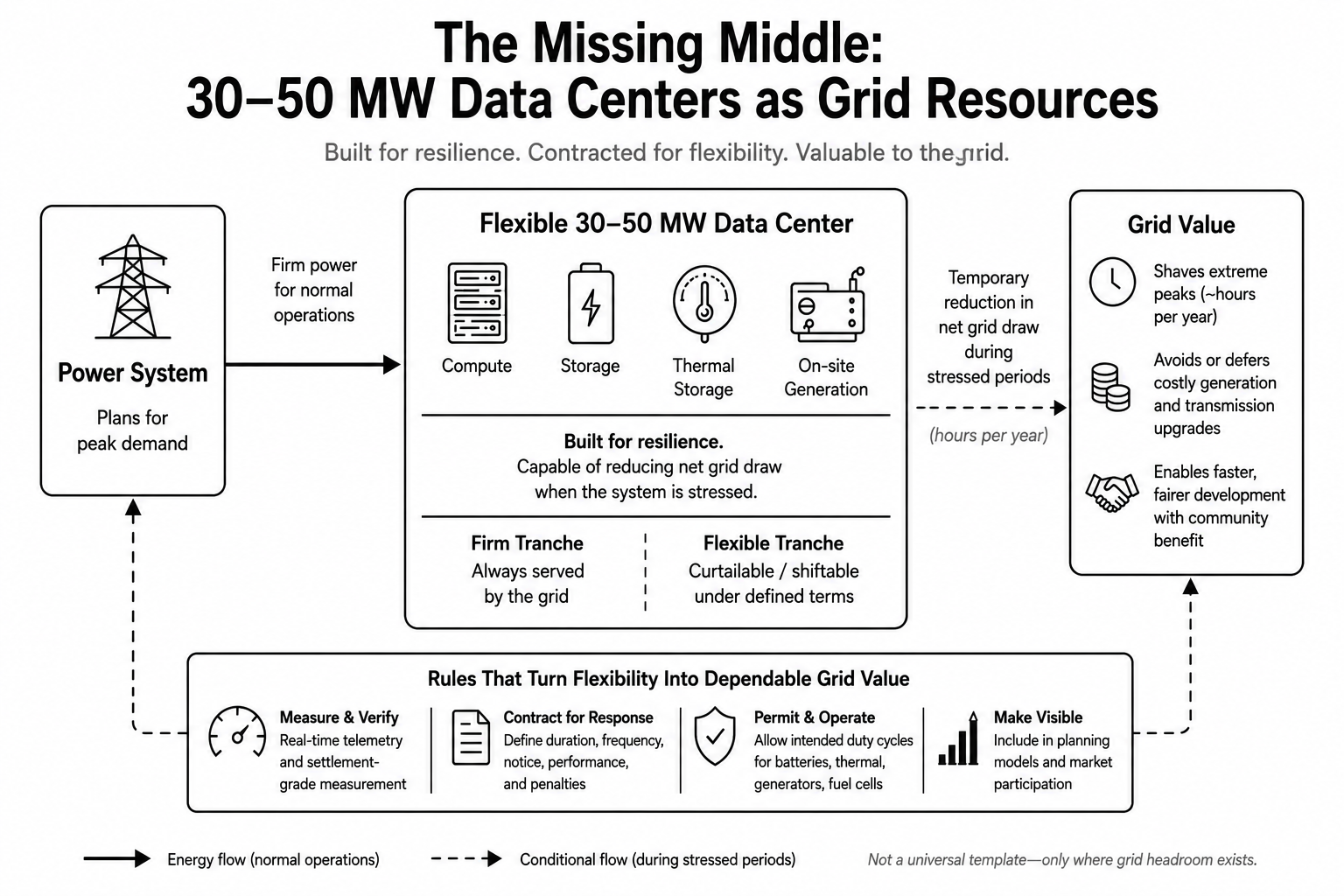

That raises a question the data center debate rarely asks: Is there a viable middle scale between small edge facilities and the campuses that now dominate headlines? Consider a 30–50 MW data center. That range is not a proven industry optimum, and it should not be treated as one. A facility of that size is still a major electric load. On a small utility system, it can be enormous. At the wrong node, it can require the same kinds of upstream upgrades that delay much larger projects. But at selected industrial sites with real distribution or subtransmission headroom, it may offer a different development path: large enough to support serious compute, small enough to be replicated across locations, and potentially flexible enough to fit the grid rather than forcing the grid to be rebuilt around it.

The real problem

A data center and its utility approach reliability from different directions. The utility plans generation and network capacity to meet the customer’s contracted service obligation. The data center operator designs site infrastructure so that an interruption upstream does not interrupt critical compute. Those are not duplicate systems performing the same job. One protects system adequacy and delivery; the other protects continuity at the facility.

That distinction matters because the strongest version of the community-scale argument is not that one of those systems is unnecessary. It is that the grid often treats the facility as a fixed, inflexible load even when the facility has multiple ways to reduce its net withdrawal during stressed hours. Those capabilities may include workload shifting, batteries, thermal storage, fuel cells, or on-site generators. Unless those capabilities are measurable, contractually committed, permitted for the intended duty cycle, and visible to planners, they cannot be relied on as system resources.

The same caution applies to data center resilience standards. Uptime Institute’s Tier framework defines performance and topology requirements, but it is technology-neutral; it does not prescribe a single universal fuel or generator configuration. Site operators also make resilience choices based on customer contracts, insurance, workload criticality, fuel logistics, and local regulation. The useful policy question is therefore not, “Why are data centers forced to buy two power systems?” It is, “Which parts of a facility’s flexibility and resilience stack can be converted into dependable grid value without compromising the function they were built to serve?”3

What the flexibility evidence shows

The case for asking that question is getting stronger. The Nicholas Institute at Duke University examined the 22 largest U.S. balancing authorities, which together represent about 95 percent of national peak load. Its 2025 study estimated 98 GW of “curtailment-enabled headroom” in a scenario limiting average annual load curtailment to 0.5 percent. In that scenario, the average balancing authority experienced some curtailment in 177 hours of the year, but most of those hours retained a substantial share of the new load, and average event duration was about 2.1 hours.4

That result is important, but its limits are equally important. The study was a first-order estimate. It did not fully model transmission constraints or every intertemporal operating constraint on the generation fleet. It does not mean that 98 GW of load can be dropped anywhere on the map without new wires or generation. It means that the power system’s extreme peaks leave a material amount of underused capacity that flexible loads may be able to access, depending on where they connect and how reliably they can respond.

The Nicholas Institute’s 2026 follow-up modeled cumulative system-cost savings of roughly $40 billion to $150 billion over the next decade under its flexibility scenarios. A separate Johns Hopkins analysis of PJM found non-firm data center service to be the largest cost lever in its scenarios, reducing total annual system costs by roughly $15–$16 billion. Both are modeled results, not observed savings. But they point in the same direction: the contractual shape of new load can matter almost as much as the magnitude of the load itself.5,6

Commercial arrangements are beginning to test that proposition. In March 2026, Google disclosed that it had integrated 1 GW of data center demand-response capacity into long-term contracts with utility partners. The company describes the capability as shifting or limiting portions of machine-learning workloads and lists agreements with Indiana Michigan Power, Tennessee Valley Authority, Entergy Arkansas, Minnesota Power, and DTE Energy. The mechanism is demand-side flexibility. It is not a fleet of backup generators selling power back to the grid.7

EPRI is trying to make such capability easier to define and plan around. Its Flex MOSAIC framework describes large-load flexibility through performance attributes such as notification time, duration, frequency of use, depth of load adjustment, ramp behavior, and availability. The program also now has a dedicated workstream on distribution-connected data centers, explicitly examining their technical, operational, interconnection, economic, and reliability requirements.8,9 This is where the community-scale concept becomes interesting. The research and early commercial deals prove pieces of the model.

Three different grid transactions

The industry often uses “flexibility” as though it were a single product. It is more useful to separate three transactions.

First, reduce grid withdrawal. A data center can shift a training run, defer batch inference, move computation to another region, discharge a battery, or temporarily reduce noncritical facility load. From the grid’s perspective, the relevant fact is the reduction in net demand. This is the domain of demand response, interruptible service, and non-firm service contracts.

Second, serve the facility behind the meter. A site can use storage or on-site generation to reduce what it draws from the utility during defined conditions. But a backup generator permitted and configured for emergencies is not automatically an economic peaker. Engine classification, emissions permits, fuel arrangements, protection systems, and tariff provisions all matter. In 2025, the U.S. Environmental Protection Agency clarified that certain emergency stationary engines may operate for up to 50 hours per year in specified non-emergency grid-reliability circumstances when defined dispatch and recordkeeping conditions are met. Duke Energy’s PowerShare Mandatory 50 program is the agency’s concrete example. That pathway is narrower than routine peak shaving, but it proves that the regulatory boundary is not simply “outage or nothing.”10

Third, export to the grid. This is a separate engineering and market transaction. A resource that energizes a facility behind the meter is not automatically authorized or technically configured to push power onto a utility feeder. Export can require a generator interconnection study, protection coordination, synchronization equipment, anti-islanding controls, telemetry, metering, dispatch rights, settlement rules, and a compensation mechanism. Depending on the arrangement, wholesale and retail jurisdiction may also divide responsibilities.

A credible community-scale model has to decide which of those three products it is selling. The strongest design may combine all three, but the contracts cannot treat them as interchangeable.

The rules are moving

Federal regulators have opened part of the door. On June 18, 2026, the Federal Energy Regulatory Commission issued tailored Section 206 show-cause orders to all six RTOs and ISOs under its jurisdiction. The Commission required the grid operators to justify their existing tariff rules or propose reforms. Among the five categories FERC identified were new transmission services for flexible large loads, treatment of co-location and behind-the-meter generation, and processes for studying generation that serves electrically proximate large loads. The action builds on FERC’s December 2025 PJM co-location order and its January 2026 approval of Southwest Power Pool’s High Impact Large Load initiative.11,12

That federal movement does not solve the community-scale problem by itself. A 30–50 MW facility may be connected to distribution or subtransmission facilities and depend heavily on state retail tariffs, utility service regulations, distribution studies, local siting approvals, and state and local air permits. The federal and state questions are therefore complementary. FERC can shape transmission service and wholesale-market treatment. State commissions and utilities still have to design workable retail service and distribution-level pathways.

The North Carolina Test case

North Carolina shows how quickly the policy pieces are moving. The governor’s Energy Policy Task Force recommended work on large-load tariffs, bring-your-own-capacity options, load flexibility, and interconnection reform. The report also documents that Duke Energy Carolinas and Duke Energy Progress already have high-load-factor tariffs available from 1 MW, with one-year terms and a minimum billing demand of 75 percent of contract capacity.13

Those existing schedules are not the end of the story. In testimony filed in late June 2026, Duke proposed a new large-load structure for customers of at least 50 MW. According to Canary Media’s review of the filing, the proposal would require a minimum payment of 75 percent and contract terms of 10 or 15 years. The commission could address the proposal in the pending rate case or open a separate docket.14

The next question for North Carolina—and for other states confronting similar growth—is whether customer protection and load flexibility can be designed together. A tariff built only around take-or-pay obligations protects existing customers from speculative load forecasts and stranded infrastructure. That matters. But a tariff that also defines a firm tranche and a measurable flexible tranche could give the utility a resource it can plan around rather than merely a customer it must build around.

What a community-scale pilot should test

The case for a community-scale data center is not strong enough to justify a nationwide template. It is strong enough to justify controlled pilots. A serious pilot would need to test the entire service architecture, not simply offer a discounted interruptible rate.

Siting discipline. Projects should be limited to nodes where utility studies show real headroom. Smaller is not automatically easier; a 40 MW load can still overwhelm the wrong feeder, substation, or local supply portfolio.

A firm and flexible load split. The service agreement should define what portion of load the utility must serve under all normal conditions and what portion can be curtailed, for how long, with what notice, and how often. Those parameters should be based on system need and facility capability, not a universal percentage copied from another jurisdiction.

Measurement and enforcement. Telemetry, automated control, periodic testing, event-performance measurement, and consequences for nonperformance are necessary if planners are going to rely on the flexible tranche.

A resource-specific resilience plan. Batteries, fuel cells, engines, thermal storage, and workload shifting have different duration, response, emissions, and fuel-security characteristics. The tariff should value delivered performance while permits and interconnection requirements remain specific to the technology.

Export as an optional separate service. Where local network studies show value, a project could test utility-controlled export under a distinct interconnection and compensation agreement. Export should not be assumed to follow automatically from behind-the-meter capability.

Ratepayer protection. Minimum bills, credit requirements, exit fees, ramp schedules, customer-funded upgrades, and transparent cost allocation remain necessary. Flexibility is not a substitute for cost causation.

Community conditions. Noise, local air emissions, water use, land use, and emergency fuel logistics should be evaluated directly. A smaller facility can reduce some impacts, but “community-scale” should describe a contract with the place, not merely a megawatt threshold.

The community-scale data center should not be sold as the answer to the data center backlash. There is no evidence yet that 30–50 MW is a universal economic sweet spot, that small utilities can absorb such loads without major upgrades, or that existing backup fleets can simply be converted into revenue-producing grid resources. Those claims require site-specific engineering, tariff analysis, permits, and project economics.

There is, however, enough evidence to support a narrower and more consequential proposition. Flexible large loads can unlock meaningful grid headroom. Non-firm service can reduce modeled system costs. Major operators are contracting for demand response at scale. Regulators are rewriting transmission rules. EPRI is developing a common vocabulary for flexibility and studying distribution-connected data centers as a distinct class. EPA has identified a limited pathway for qualifying backup engines to support local reliability.

The pieces are emerging. What does not yet exist at scale is the integrated package: a modestly sized data center at a location with real grid headroom; a retail tariff that distinguishes firm from flexible demand; a facility designed to deliver that flexibility; a legally usable behind-the-meter resource stack; and, where it is technically valuable, a separate pathway for controlled export.

That is the experiment worth running. The next useful data center may not be the largest one a developer can finance or the smallest one a community will tolerate. It may be the one whose contract tells the truth about what the grid must serve, when the facility can move, and what the site can reliably give back.

Notes

2. Data Center Watch, “Q1 2026: Data Center Watch Report,” 2026.

3. Uptime Institute, “Tier Classification System,” accessed July 8, 2026.

8. Electric Power Research Institute, “Flex MOSAIC,” DCFlex, 2026.

13. North Carolina Energy Policy Task Force, Interim Report, February 2026.

Bibliography

Data Center Watch, “Q1 2026: Data Center Watch Report,” 2026.

Electric Power Research Institute, “Flex MOSAIC,” DCFlex, 2026.

Michael Terrell, “A New Milestone for Smart, Affordable Electricity Growth,” Google, March 19, 2026.

North Carolina Energy Policy Task Force, Interim Report, February 2026.

Uptime Institute, “Tier Classification System,” accessed July 8, 2026.